Health insurance experts reveal key considerations for Britons exploring private healthcare options

Key findings:

- Health insurance specialists outline five crucial factors to consider when choosing private medical coverage

- Checklist includes understanding policy exclusions, waiting periods, and the impact of pre-existing conditions

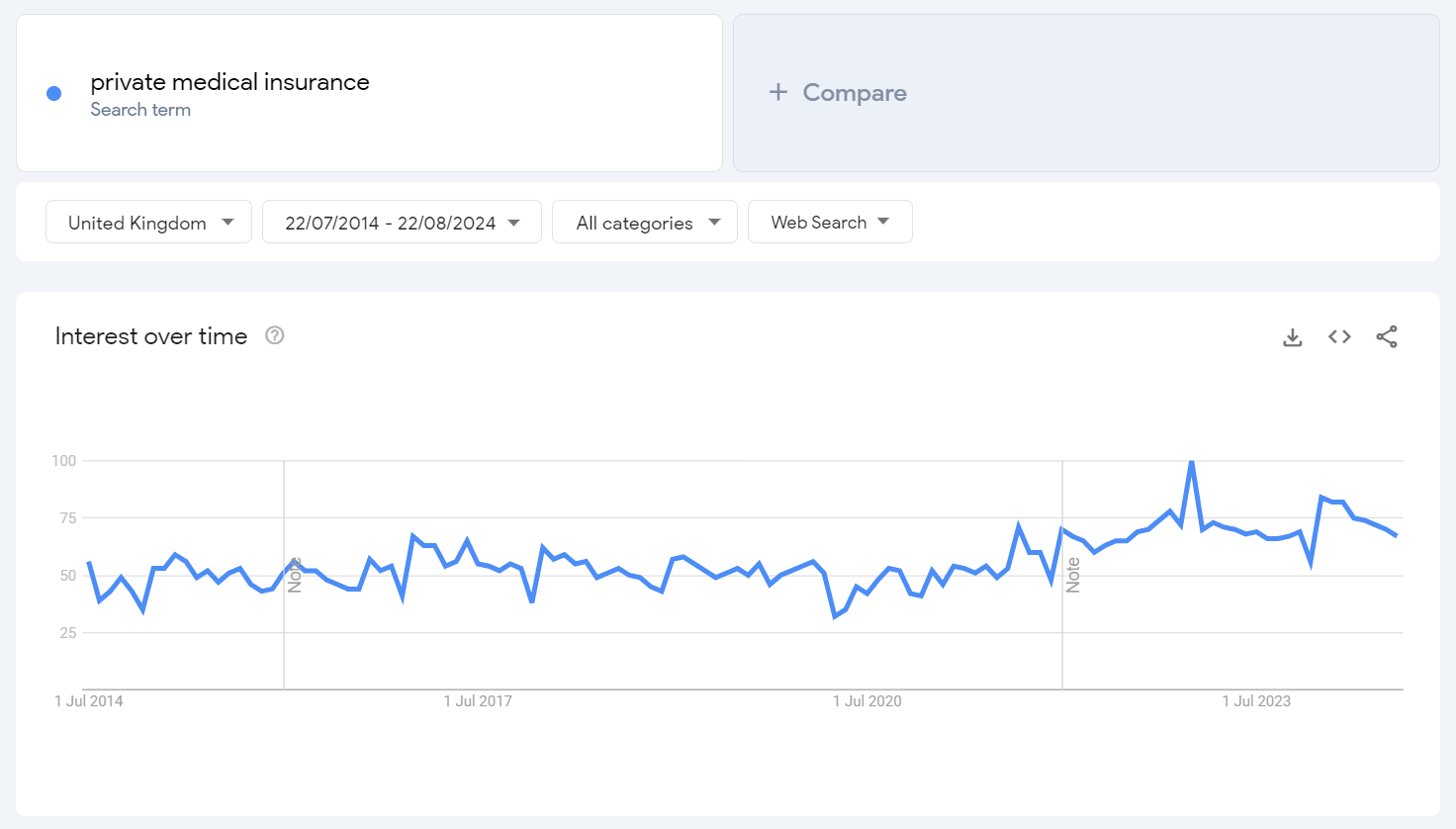

- Recent data shows a growing interest in private medical insurance among UK residents

As NHS wait times get longer and certain needs need to be met, many people in the UK are deciding to get private medical insurance for certain types of care. With private care, you are more likely to get appointments quickly and you won’t have to wait months or even years for medical procedures.

Here is a list of the five most important things to check with your provider before deciding to sign up for private medical insurance.

- Policy exclusions and limitations

Before signing up for any private medical insurance, it’s important to understand what is and isn’t covered. Many policies have specific exclusions or limitations that could significantly impact your coverage.

Start by requesting a comprehensive list of exclusions from your potential provider. Pay close attention to coverage for specific treatments or conditions you’re particularly concerned about. For instance, some policies might exclude certain types of cancer treatments or have limitations on mental health coverage.

Additionally, understand any monetary limits on certain treatments or overall annual coverage. According to the Association of British Insurers, the average claim paid on private medical insurance policies in 2020 was £2,000, but individual claims can vary widely depending on the treatment required.

- Waiting periods

Most private medical insurance policies have waiting periods before you can claim for certain conditions or treatments. These periods can vary significantly between providers and types of coverage. Confirm the general waiting period for new policies, which typically ranges from 14 to 30 days.

However, be aware that there might be different waiting periods for specific conditions or treatments. For example, some policies may have longer waiting periods for pregnancy-related claims or certain elective procedures.

Understanding how waiting periods might affect any ongoing health concerns is crucial. If you’re switching providers, ask about the possibility of having waiting periods waived, especially if you’ve already served them with your previous insurer.

- Impact of pre-existing conditions

Pre-existing conditions can significantly affect your coverage and premiums. It’s essential to disclose all pre-existing conditions honestly during the application process. Ask your potential provider how each condition might impact your coverage and premiums.

Some insurers use a ‘moratorium’ underwriting approach, where pre-existing conditions from the past five years are initially excluded but may be covered after a symptomless and medication-free period, typically two years.

Others may use ‘full medical underwriting’, which requires a detailed medical history and may result in permanent exclusions for certain conditions. Understand if and when pre-existing conditions might be covered in the future, and how this could affect your long-term healthcare strategy.

- Outpatient coverage and limits

Outpatient coverage is a crucial aspect of private medical insurance policies in the UK. This type of coverage includes consultations, diagnostic tests, and treatments that don’t require hospital admission.

Most policies offer different levels of outpatient coverage. Some may provide full coverage with no monetary limits, while others might set annual caps on outpatient claims. These limits can range from a few hundred to several thousand pounds per year.

When reviewing policies, check the outpatient allowance and understand what it covers. Common outpatient services include specialist consultations, physiotherapy, diagnostic scans (like MRIs or CT scans), and certain treatments such as chemotherapy.

Some insurers might fully cover specific outpatient treatments (like cancer care) regardless of general outpatient limits.

- Premium increases and policy renewals

Understanding how your premiums might change over time is crucial for long-term planning. Ask about the factors that could lead to premium increases, such as age, claims history, or general inflation in healthcare costs.

Understand how making claims might affect future premiums – some insurers offer no-claims discounts, while others may increase premiums following significant claims. Clarify the renewal process and any guaranteed insurability provisions. Some policies may allow you to renew regardless of any changes in your health, while others may reassess your risk at each renewal.

When choosing private medical insurance, it’s essential to look beyond the headline premium and carefully consider these five key factors.

Before making the decision to get private medical insurance, remember to ask a lot of questions of the different providers and make an informed decision based on these expert tips. Don’t forget to ask for a list of benefits, premium prices, exclusions, and different types of policies when you are comparing different medical insurance providers.

Remember that policies can vary significantly between providers, so take the time to compare options and ask detailed questions before committing to a plan. You can find out more about private medical insurance at Usay Compare.

ENDS

If you would like to use this information, could you please include a link to the Usay Compare website, (https://www.usaycompare.co.uk )? This will help us to continue to provide quality content.

About Usay Compare

Usay Compare is a leading online health insurance comparison service in the UK. They provide impartial advice and comparisons for various health insurance products, helping individuals and families find the most suitable coverage for their needs.

Methodology

1. Association of British Insurers: UK Insurance and Long-Term Savings Key Facts

2. Searches for ‘private medical insurance’ see a steady rise over the past 10 years: